Boat Rental Business Insurance: What Coverage Do You Actually Need

Starting a boat rental company is an exciting venture. You get to share your passion for the water with locals and tourists alike. However, the open water is unpredictable. If you do not have proper boat rental business insurance, one bad accident can end your business quickly. This guide will help you understand the protection you need to stay safe and profitable.

Many new owners wonder if they need special policies for their fleet. The short answer is yes. Standard policies simply do not cover commercial rental activities. To operate a successful fleet, you must understand your boat rental business insurance requirements. This post will break down the essential coverage types, costs, and strategies to keep your business secure.

The Profitability Question: Is Boat Rental Business Insurance Profitable?

New entrepreneurs often ask: is boat rental business insurance profitable? It is natural to look at insurance premiums as a burden on your cash flow. However, you should view insurance as a strategic investment in your longevity.

If you lack adequate coverage, a single lawsuit or stolen vessel could wipe out your annual gains. When you manage risk correctly, you protect your boat rental business insurance profit margin, which typically ranges between 35% and 45% for healthy fleets. Essentially, insurance acts as a safety net that keeps your business running year after year. Without this safety net, you are gambling with your entire investment every time a customer leaves the dock.

Essential Coverage: Liability Insurance for Boat Rentals

When you lease out watercraft, you are not just renting equipment. You are providing a service that involves significant public risk. If you want a broader view of coverage options across different rental niches, our 5 Best Insurance Policies For Rental Businesses breaks down which policies matter most and why. This is why liability insurance for boat rentals is the most critical component of your risk management strategy.

1. Protection and Indemnity (P&I)

P&I insurance is a specialized form of marine liability coverage. It protects you if a customer is injured while on your boat. It also covers damages you might cause to other people’s property, such as another boat, a dock, or marina infrastructure. In the maritime world, this is non-negotiable.

2. Commercial Hull Insurance

Your boats are high-value assets. Commercial hull insurance covers the cost to repair or replace your vessels. This includes damage from storms, collisions with underwater hazards, or theft. Unlike standard auto insurance, marine hull policies are specific to the water and account for unique risks like sinking or engine submersion.

3. Medical Payments Coverage

Even if you are not at fault, accidents happen. Medical payments coverage helps cover the cost of immediate medical care for a customer who gets hurt on your vessel. This can prevent small incidents from turning into massive lawsuits.

Understanding Boat Rental Business Insurance Cost

Determining your boat rental business insurance cost depends on several specific factors. Insurance companies look at your total fleet value, the type of boats you own, and your location.

-

Fleet Value: The more expensive your boats are, the higher your premiums will be. Replacing a $100,000 yacht costs more than replacing a $15,000 jet ski.

-

Operating Location: Regions with frequent storms or crowded waterways may result in higher rates. Insurers assess the risk of your specific environment.

-

Safety History: If you have a clean record with few claims, your premiums will likely be lower. Insurance companies reward operators who take safety seriously.

-

Deductibles: Choosing a higher deductible can lower your monthly premium. However, you must ensure you have enough cash on hand to cover that deductible if an accident occurs.

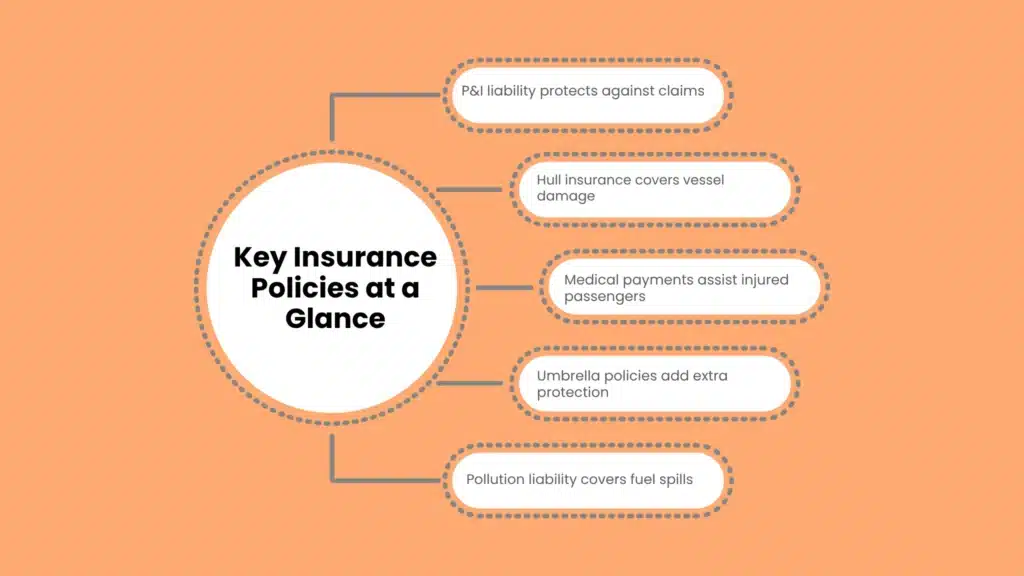

Key Insurance Policies at a Glance

To make sense of the different options, review the table below. This will help you identify the primary purpose of each policy type.

| Insurance Type | Primary Purpose | Risk Level Covered |

| P&I Liability | Protects against bodily injury and third-party property damage. | High (Essential for all operators) |

| Commercial Hull | Covers the cost to repair or replace your physical boats. | High (Essential for asset protection) |

| Medical Payments | Covers immediate medical costs for injured passengers. | Moderate (Helps avoid lawsuits) |

| Umbrella Policy | Provides extra liability coverage above your base limits. | Low (Recommended for larger fleets) |

| Pollution Liability | Covers costs if your boat leaks fuel into the water. | Moderate (Required in many marinas) |

Requirements for Getting Insured

Securing the right policy requires preparation. Insurance underwriters are cautious. For a closely related walkthrough of legal and insurance prerequisites in a similar water-based rental niche, see our Kayak Rental Business Legal Requirements & Permits guide. To meet all boat rental business insurance requirements, you must follow these steps carefully.

Protecting Your Business from Theft by Conversion

One specific risk in the boat rental industry is theft by conversion. This occurs when a customer signs a valid lease agreement but then refuses to return the boat.

Because you technically handed over the keys voluntarily, standard theft policies might not cover this. Therefore, you must specifically ask your broker for a conversion endorsement. This protects you if a renter decides to steal your boat.

Additionally, you should require a security deposit authorization on the customer’s credit card before they leave. This simple step often discourages bad actors from targeting your fleet. It also provides you with financial leverage if the boat returns with minor damages.

Expert Tips to Manage Insurance Costs

Managing costs is vital for long-term success. You can control your expenses without sacrificing safety. These same cost-control principles apply across the broader watercraft rental space, as we cover in How To Start A Paddle Boat Rental Business, where insurance and safety spending directly affect margins.

-

Offer Damage Waivers: This is a brilliant way to increase revenue. Charge customers a fee to waive their liability for minor scratches or mechanical issues. This often offsets your insurance premium costs.

-

Use GPS Monitoring: Insurance carriers view GPS data favorably. If you can prove you monitor vessel location and speed, you may qualify for a lower rate.

-

Require Safety Certification: Mandate that all renters complete a short safety course. This reduces the likelihood of accidents. Consequently, it lowers your claims frequency.

-

Audit Your Policy Annually: As your business grows, your needs will change. Review your coverage every year to ensure you are not paying for protection you no longer need.

Conclusion

Boat rental business insurance is not just a regulatory requirement. It is the foundation of a sustainable business. By investing in proper liability insurance for boat rentals, you shield your hard-earned assets from the risks of the water.

Remember to partner with an expert, maintain your fleet, and use clear contracts. These steps will keep your premiums manageable and your business secure. When you handle these requirements early, you gain the peace of mind to focus on what you love most: helping your customers enjoy their time on the water.

For more hands-on business blueprints, rental checklists, and operational guides built for modern entrepreneurs, explore our full library of resources at reliablestartup.com.

Frequently Asked Questions

Is boat rental business insurance profitable in the long run?

Yes. While it is an ongoing cost, it protects your capital. A single major accident without insurance could bankrupt your business. Therefore, it is a necessary expense for long-term profitability.

What happens if a customer has an accident while drunk?

Your rental contract should strictly forbid alcohol consumption. If a customer ignores this, your insurance company may deny the claim. Consequently, you must enforce a zero-tolerance policy at your dock.

Can I use my personal boat insurance for rentals?

Absolutely not. Personal boat insurance is strictly for private use. If you rent out your boat, your personal policy will likely be void. You need a dedicated commercial marine policy.

What is the difference between hull coverage and liability coverage?

Hull coverage pays for damage to your boat. Liability coverage pays for damages or injuries caused to other people or their property. You need both to be fully protected.

How often should I check my safety equipment?

Check your safety gear before every single rental. Ensure life jackets are in good condition and fire extinguishers are fully charged. Proper maintenance records can help you during insurance claims.