Vacation Rental Business Taxes: A Beginner’s Guide

The short-term lodging market continues to grow rapidly today. Therefore, entering the hospitality space offers a reliable and lucrative opportunity for property owners. Think about it realistically. Travelers and families rarely want to spend thousands of dollars staying in cramped, sterile hotel rooms for a week-long holiday. Instead, they look for a comfortable local home to rent.

For an ambitious real estate investor, mastering your vacation rental business taxes makes perfect sense. Starting with a clear understanding of your tax responsibilities forces you to structure your bookkeeping correctly from day one. Consequently, this organized approach allows you to shelter your revenue legally and fund your future property expansions out of actual savings. In this comprehensive guide, we will break down exactly how federal and local lodging assessments impact your operations. Additionally, we will dive deep into standard tax deductions for vacation rentals, analyze your total annual compliance expenses, and look closely at the math to answer the big question: is vacation rental business taxes profitable?

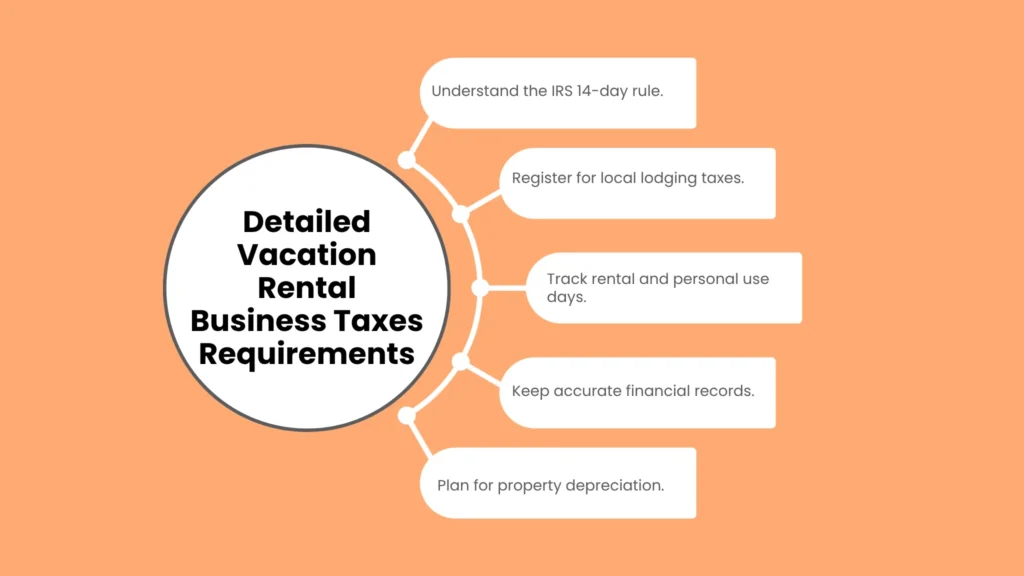

Detailed Vacation Rental Business Taxes Requirements

You do not need to hire an expensive corporate accounting firm to manage your properties right away. Similarly, you do not need a degree in finance to track your nightly income. However, you must meet a specific set of foundational tax guidelines. If you’re still setting up your listing, our guide on how to start a vacation rental business covers the foundational steps before tax season even becomes a concern. Skipping over your local lodging registrations to save time early on is a dangerous trap. It can easily result in heavy audit penalties, which can end your business before it even starts. To operate with confidence, you must satisfy a few basic vacation rental business taxes requirements to protect your brand and your personal wealth.

1. The 14-Day IRS Tax Rule Threshold

Before you file your annual tax return, you must understand the exact classification of your property. The IRS draws a very sharp line based on how many days you rent out the home each year. If you rent out your property for 14 days or fewer, you do not have to report any of that rental income on your federal return. This strategy represents a massive tax loophole for occasional hosts.

However, if you rent out the home for 15 days or more, you must report every single dollar of gross income. Additionally, you must divide your expenses carefully between personal use days and active rental days. Keeping detailed calendar records is mandatory because the IRS will completely reject your expense write offs if you cannot prove the exact days your property was occupied by paying guests. For the official rules on this threshold, the IRS Topic No. 415 on renting residential and vacation property outlines exactly how the 14-day rule and personal-use limits are applied.

2. State and Local Occupancy Tax Collections

You absolutely cannot ignore municipal lodging assessments when managing your operating costs. In the short-term rental space, local taxes are an inescapable daily reality. Your city, county, or state will charge a transient occupancy tax (TOT), which usually ranges from 5% to 15% of your nightly rate.

Therefore, you must verify whether your booking platforms, like Airbnb or VRBO, collect and remit these local lodging taxes automatically on your behalf. Fortunately, setting up automated collection in your platform portal is quite simple. However, checking your regional county clerk requirements is mandatory because failing to register your lodging permit can cause local authorities to shut down your listing completely. Beyond taxes, your guest agreements also need to hold up legally our lease agreements guide explains what every rental contract should include.

3. Structural Depreciation Asset Accounting

Your long-term property write-off strategy stands as the most important behind-the-scenes part of your tax shield. You need to account for the natural wear and tear of the building structure over time. The IRS allows you to deduct the value of your residential rental building over a standard 27.5-year lifespan.

Furthermore, you should consider a professional cost segregation study for high-value properties. This accounting technique accelerates your deductions on interior items like appliances, carpeting, and furniture, allowing you to claim massive upfront tax write-offs during your earliest, most critical years of operation. If you’re deciding between renting long term or seasonally, our comparison of short-term vs long-term rental business models breaks down which approach maximizes both cash flow and depreciation benefits.

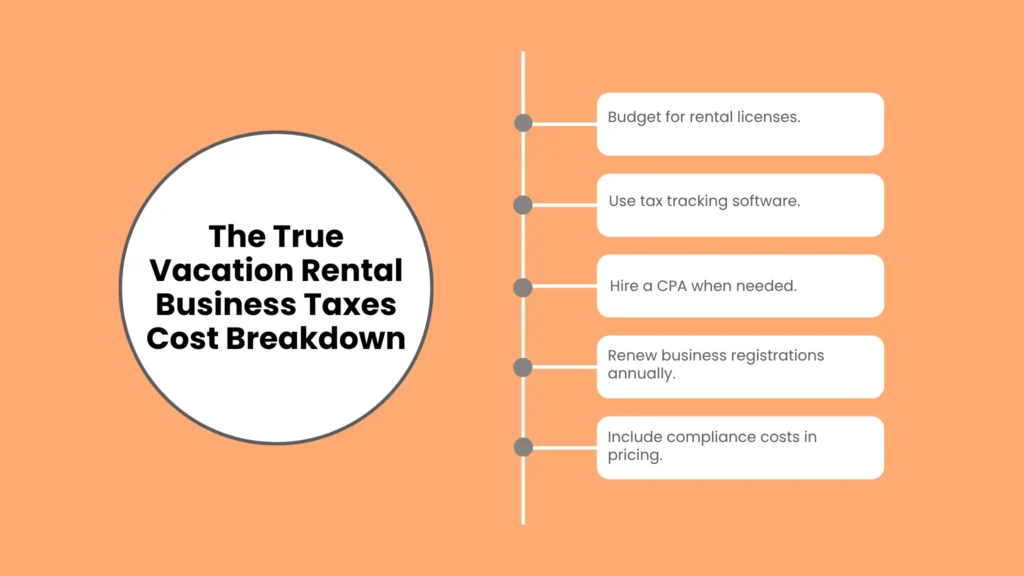

The True Vacation Rental Business Taxes Cost Breakdown

How much capital do you realistically need to allocate for tax prep, licenses, and filings each year? The total volume depends entirely on your property location and your booking software. If you attempt to track multiple properties manually on paper, your accounting errors will surge.

However, if you use automated tracking tools and a qualified local CPA, your annual compliance expenses stay highly manageable. Let’s take a look at a realistic financial breakdown of your estimated annual vacation rental business taxes cost items.

Estimated Annual Tax Compliance and Operational Fees

| Expense Category | Single Property Lean Setup | Multi-Property Scaling Setup | Who You Pay |

| Short-Term Rental Lodging License | $50 to $150 | $200 to $500 | City or County Clerk |

| Automated Tax Tracking Software | $0 to $120 | $200 to $450 | Accounting SaaS Providers |

| Professional CPA Tax Preparation | $300 to $600 | $800 to $2,000 | Certified Public Accountant |

| Transient Occupancy Tax (TOT) | Built into Guest Fees | Built into Guest Fees | State & Local Revenue Dept. |

| LLC Business Registration Renewal | $50 to $300 | $100 to $600 | Secretary of State |

| Total Annual Compliance Budget | $450 to $1,170 | $1,300 to $3,550 | Total Compliance Cash Needed |

Based on available industry data from successful property managers, factoring these compliance expenses directly into your nightly rate allows you to achieve profitability very quickly. By maintaining an accurate ledger early on, you ensure that every single deduction goes toward paying off your initial operational overhead.

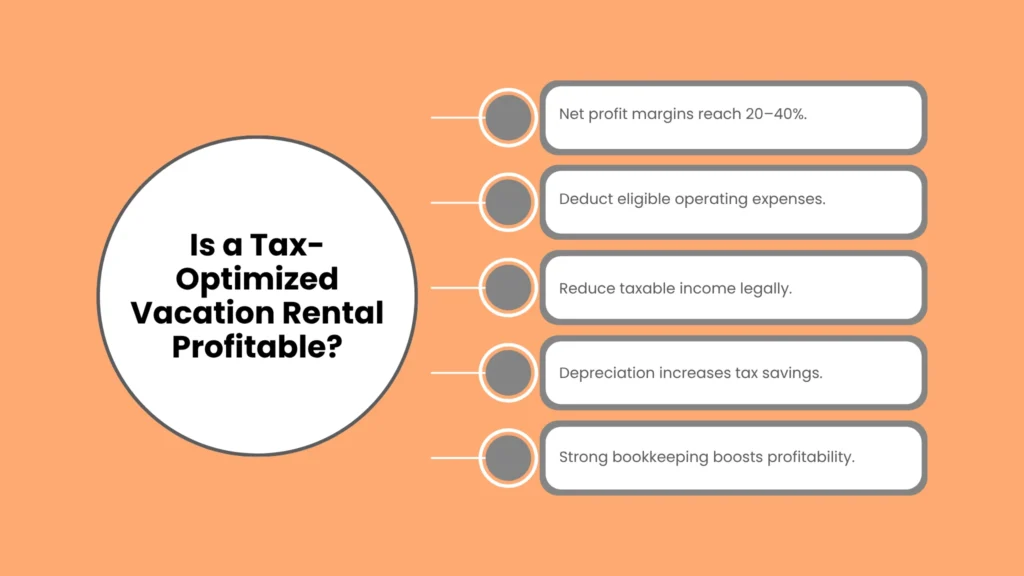

Is a Tax-Optimized Vacation Rental Profitable?

Prospective investors frequently look at rising local lodging assessments and ask: is vacation rental business taxes profitable once you pay all your fees? The answer becomes obvious once you look at the math behind strategic real estate write-offs and asset utilization.

Unlike a traditional corporate salary where your income is taxed immediately before you touch it, a real estate rental business allows you to subtract a massive list of operational expenses before calculating your net taxable income.

Your Expected Vacation Rental Business Taxes Profit Margin

A well-run short-term property can achieve an outstanding net vacation rental business taxes profit margin of 20% to 40% after adjusting for write-offs. If you claim all eligible deductions legally and track your utility bills accurately, your taxable income remains virtually nonexistent. This allows your net cash flow margins to surge higher than traditional investments.

Most baseline operating expenses like property management fees, internet subscriptions, landscaping, and professional cleaning costs are completely deductible. Once your property clearances clear your mortgage interest and structural depreciation floors, your business generates pure, tax-sheltered cash flow.

Strategic Real-World Tax Deductions

Let’s look at a simple, real-world example of an optimized property ledger. Suppose your beach condo generates $35,000 in gross booking revenue over a summer season. If your mortgage interest, property taxes, cleaning fees, and utilities total $22,000, your raw cash profit sits at $13,000. However, after your CPA applies an additional $8,000 for building depreciation and asset write-offs, your taxable net income drops to just $5,000.

Consequently, you keep the full cash profit in your bank account while paying income taxes on a tiny fraction of that amount. As your portfolio grows, you can easily reinvest those tax savings into high-margin property additions, turning a single asset into a highly profitable multi-property rental empire.

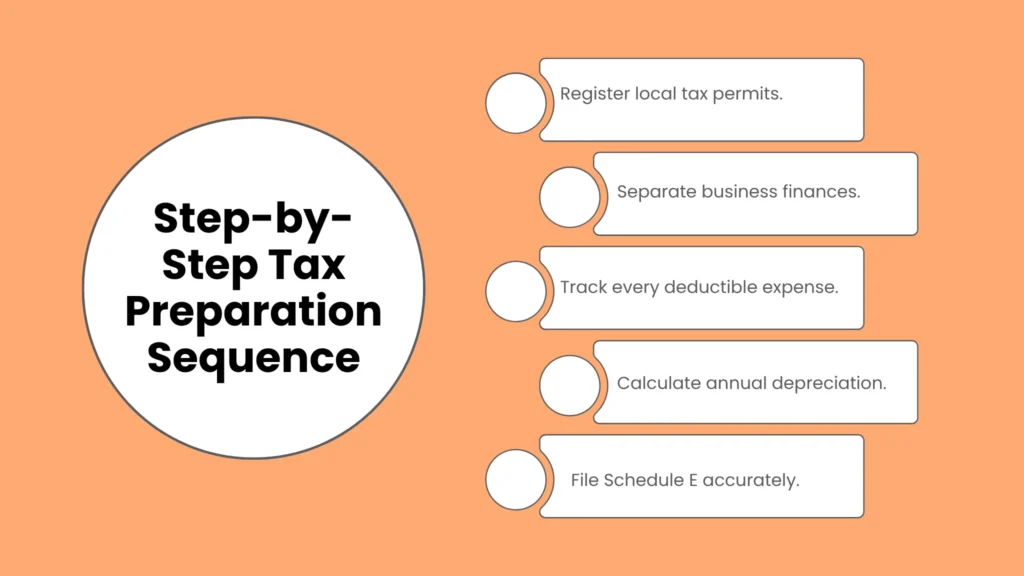

Step-by-Step Tax Preparation Sequence

To organize your property bookkeeping without making costly compliance mistakes or getting overwhelmed by receipts, follow this clear chronological order to secure a stress-free tax filing.

Common Rental Tax Pitfalls to Avoid

The biggest mistake new property owners make is failing to track their personal use days accurately. You do not need to live on the property full-time, but you must monitor your stays. Many beginners successfully use their beach house or mountain cabin for personal vacations without logging the time. For hosts renting out cabins specifically, our dedicated guide on starting a cabin rental business covers similar personal-use tracking rules in more detail. If your personal use exceeds 14 days or 10% of the total rented days, the IRS will completely reclassify your property as a personal residence, which destroys your ability to deduct net operational business losses.

Another critical error is neglecting to document travel expenses to your rental property. Driving out to inspect your cottage or perform routine maintenance counts as an eligible business trip. Therefore, you must establish a strict mileage log detailing the date, destination, and business purpose of every single drive. Additionally, keep your fuel and highway toll receipts to claim your full deduction at the end of the year.

Closing Thoughts on Tax Strategy

Building a successful short-term lodging brand remains one of the most accessible, high-yielding paths to long-term real estate wealth. By narrowing your focus to high-yield tourist markets, keeping your operational bookkeeping flawless, and utilizing strategic tax deductions to shield your earnings, you can build a highly resilient business. Focus on providing an exceptional guest experience and tracking your expenses precisely. Consequently, your property will naturally generate the revenue required to scale your venture.

If you are looking for practical tax checklists, downloadable bookkeeping templates, and operational blueprints to grow your lodging company, explore our complete start-up library at reliablestartup.

Frequently Asked Questions

What are the most profitable tax deductions for vacation rentals?

While standard cleaning and utility costs are helpful, structural depreciation, mortgage interest deductions, and local property taxes offer the highest long-term financial relief for hosts. They allow you to offset massive chunks of your active booking income without spending any extra out-of-pocket cash.

How do I handle lodging taxes if I use automated booking platforms?

In most tourist regions, major listing platforms collect transient occupancy taxes directly from the guest at checkout and remit them to the local government automatically. However, you must inspect your account settings carefully. If your local municipality does not have an active collection agreement with the platform, you are fully responsible for calculating and paying those lodging taxes yourself.

Can I write off the furniture and design decor I buy for the property?

Yes. Any asset you purchase to fully furnish or style your guest space, including sofas, mattresses, smart TVs, and kitchenware, is completely deductible. You can choose to write off the entire cost in a single year using Section 179 bonus depreciation, or spread the deduction out over a standard five-to-seven-year asset lifespan.

What happens if my vacation rental business shows a net financial loss?

If your rental expenses and depreciation exceed your gross booking revenue, your business has generated a passive loss. If your adjusted gross income sits below $100,000, you can generally deduct up to $25,000 of these rental losses against your regular active job income, providing a fantastic annual tax break.