Unsecured Business Funding for Startups: No Collateral

Unsecured business funding for startups is one of the fastest ways to access capital without putting up collateral.

If you’re building a new venture, this funding can help you move quickly while keeping your personal and business assets protected.

However, “unsecured” doesn’t mean “no rules.”

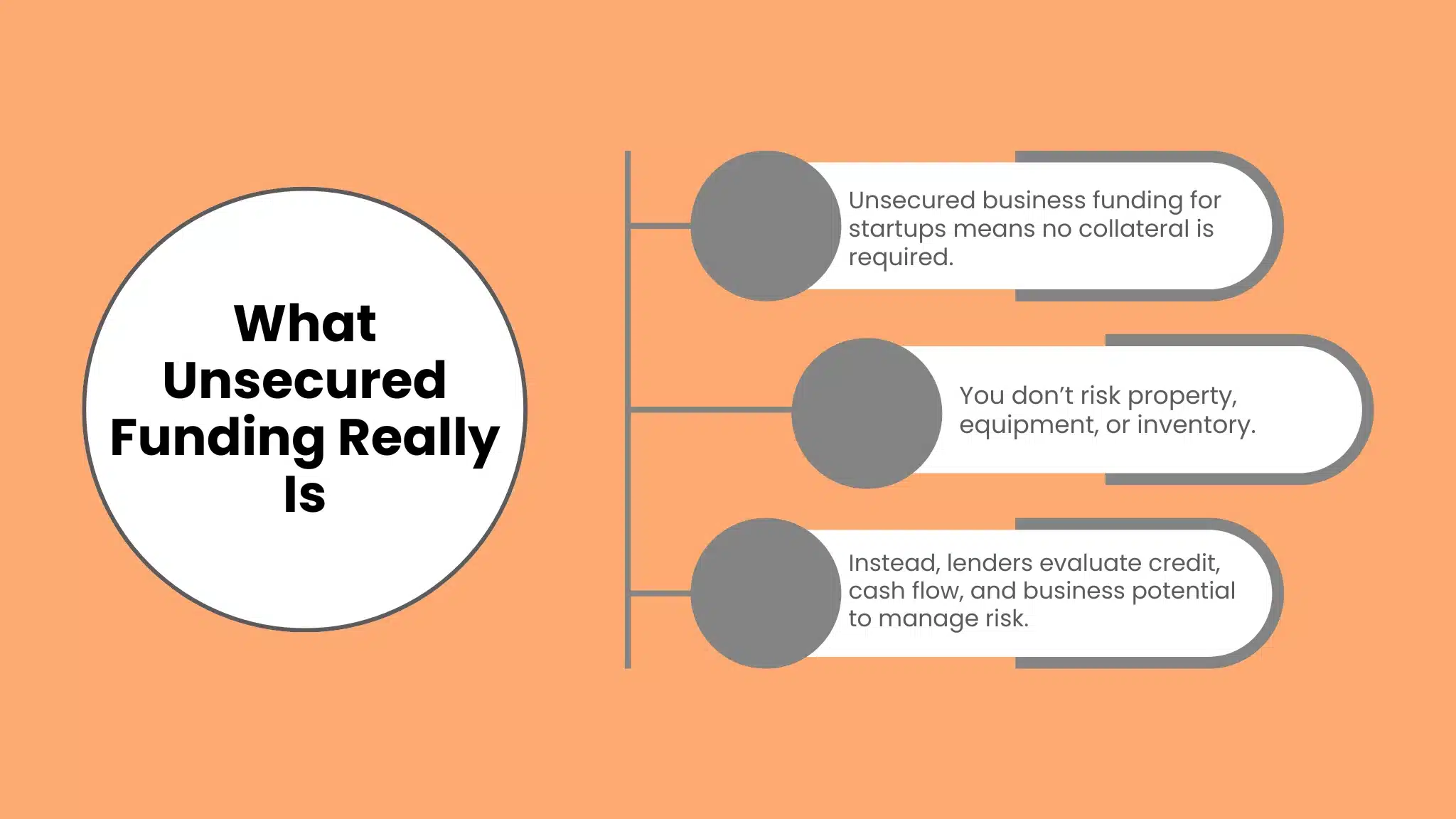

Instead, lenders and funding providers look at other signals like revenue, cash flow, credit, and business potential.

In this guide, you’ll learn what unsecured funding really is, how it works, and which options fit different startup stages.

Plus, you’ll get clear tips to improve approvals and avoid expensive mistakes.

What unsecured startup funding actually means

Unsecured funding means you don’t pledge specific collateral like property, equipment, or inventory.

Even so, providers still manage risk through credit checks, pricing, and approval conditions.

For example, some lenders rely on personal credit when a startup is brand new.

Meanwhile, others focus on revenue trends once the business is actively selling.

Because there’s no collateral, unsecured funding can feel less stressful.

At the same time, it can be more selective, and sometimes more expensive, depending on your profile.

Why startups choose unsecured funding

Startups often need speed and flexibility, and unsecured funding can deliver both.

Also, it can fill gaps when traditional banks say “no” due to limited history.

Here are common reasons founders prefer unsecured options:

-

You want to avoid risking assets like a home or vehicle.

-

You need funding quickly for marketing, inventory, or hiring.

-

You’re still early-stage and don’t have collateral to pledge.

-

You want multiple funding sources instead of one big loan.

Still, it’s smart to compare total cost, not just the monthly payment.

Otherwise, a “quick win” today can become a cash-flow problem later.

Best types of unsecured business funding for startups

Different options work better at different stages.

So, choose based on whether you have revenue, strong credit, or a clear repayment plan.

Business credit cards and charge cards

Business cards are a popular unsecured option because approvals can be fast.

Additionally, many cards offer rewards and short-term flexibility.

However, rates can be high if you carry balances month to month.

So, it’s best to use cards for predictable expenses you can repay quickly.

Unsecured term loans

Unsecured term loans provide a lump sum and fixed repayment schedule.

Therefore, they can be ideal for planned purchases like equipment, website development, or hiring.

Even so, startups may face stricter approval requirements.

Typically, stronger personal credit and stable income signals help a lot.

Lines of credit: Unsecured Business Funding for Startups

A line of credit gives you access to a pool of funds you can draw from as needed.

As a result, it’s great for managing cash flow swings, especially in growing startups.

Moreover, you only pay interest on what you use.

Still, approval may depend on revenue, bank statements, or credit score.

Revenue-based financing

Revenue-based financing (RBF) is designed for startups with consistent sales.

Instead of fixed payments, repayments are often tied to revenue performance.

Because of that, this option can feel less intense during slower months.

On the other hand, the total cost can be higher, so you must review the terms carefully.

Invoice financing: Unsecured Business Funding for Startups

If your startup sells B2B and invoices customers, invoice financing can unlock cash sooner.

In other words, you get funding against outstanding invoices rather than waiting 30–90 days.

This can improve working capital quickly.

However, fees vary, and it’s important to understand how collections are handled.

Merchant cash advances (use with caution)

Merchant cash advances are based on card sales and repay through daily or weekly deductions.

They can be easy to access, yet they often come with high effective costs.

So, they’re usually a last-resort option.

If you use one, keep the amount small and the payoff timeline short.

What lenders look for when there’s no collateral

When collateral isn’t part of the deal, providers look at risk in other ways.

So, understanding these factors helps you prepare and apply smarter.

Common approval factors include:

-

Personal credit score and credit history

-

Monthly revenue and consistency (if you’re already selling)

-

Bank statement health and cash flow patterns

-

Time in business and industry risk

-

Existing debt and payment performance

-

Business plan clarity for some startup-focused programs

Even if you’re early, you can still improve your profile.

For example, clean financial records and steady deposits build confidence fast.

How much unsecured funding can a startup get?

The amount depends on your stage and strength of your financial signals.

Generally, newer startups with no revenue may qualify for smaller limits first.

In contrast, revenue-generating startups can qualify for higher amounts.

Also, stacking multiple products—like a card plus a line of credit—may increase total access.

Still, bigger isn’t always better.

Instead, borrow what you can comfortably repay without choking growth.

Pros and cons you should know before applying

Unsecured funding can be powerful, but you should see the full picture.

So, consider both the advantages and tradeoffs.

Pros:

-

No collateral required

-

Often faster approval and funding

-

Flexible use of funds

-

Can help build business credit over time

Cons:

-

May require strong personal credit early on

-

Rates or fees can be higher than secured loans

-

Some products have frequent repayments

-

Limits may start small until you prove performance

Therefore, your best move is to match the funding type to your cash-flow reality.

That way, the funding supports growth instead of creating stress.

Step-by-step: how to qualify faster

If you want better approvals and terms, preparation matters.

Fortunately, small upgrades can make a big difference.

1) Organize your financial documents

Keep your bank statements, revenue records, and expense tracking clean.

Also, separate business and personal finances as early as possible.

2) Build business credibility signals

Use a consistent business name, professional email, and clear service description.

Moreover, have basic documentation ready, like business registration and tax IDs where applicable.

3) Improve credit the smart way

Pay bills on time and reduce credit utilization when possible.

Additionally, avoid multiple applications in a short period because it can lower your score.

4) Start with realistic amounts

Apply for funding that matches your current ability to repay.

Then, after consistent payments, request increases or better terms.

5) Choose the right product for your use case

If you need ongoing working capital, a line of credit may fit.

Meanwhile, if you need a one-time push, a term loan might be better.

Smart ways to use unsecured startup funding

Funding works best when it fuels growth that pays back the cost.

So, focus on uses with measurable return.

Great uses include:

-

Launch marketing with trackable acquisition costs

-

Inventory that sells quickly and consistently

-

Hiring for revenue-driving roles, like sales or customer success

-

Tools that reduce labor time and improve delivery

-

Short-term cash-flow bridging while you grow recurring revenue

On the other hand, avoid using funding for vague spending.

For example, “general expenses” without a plan can drain capital fast.

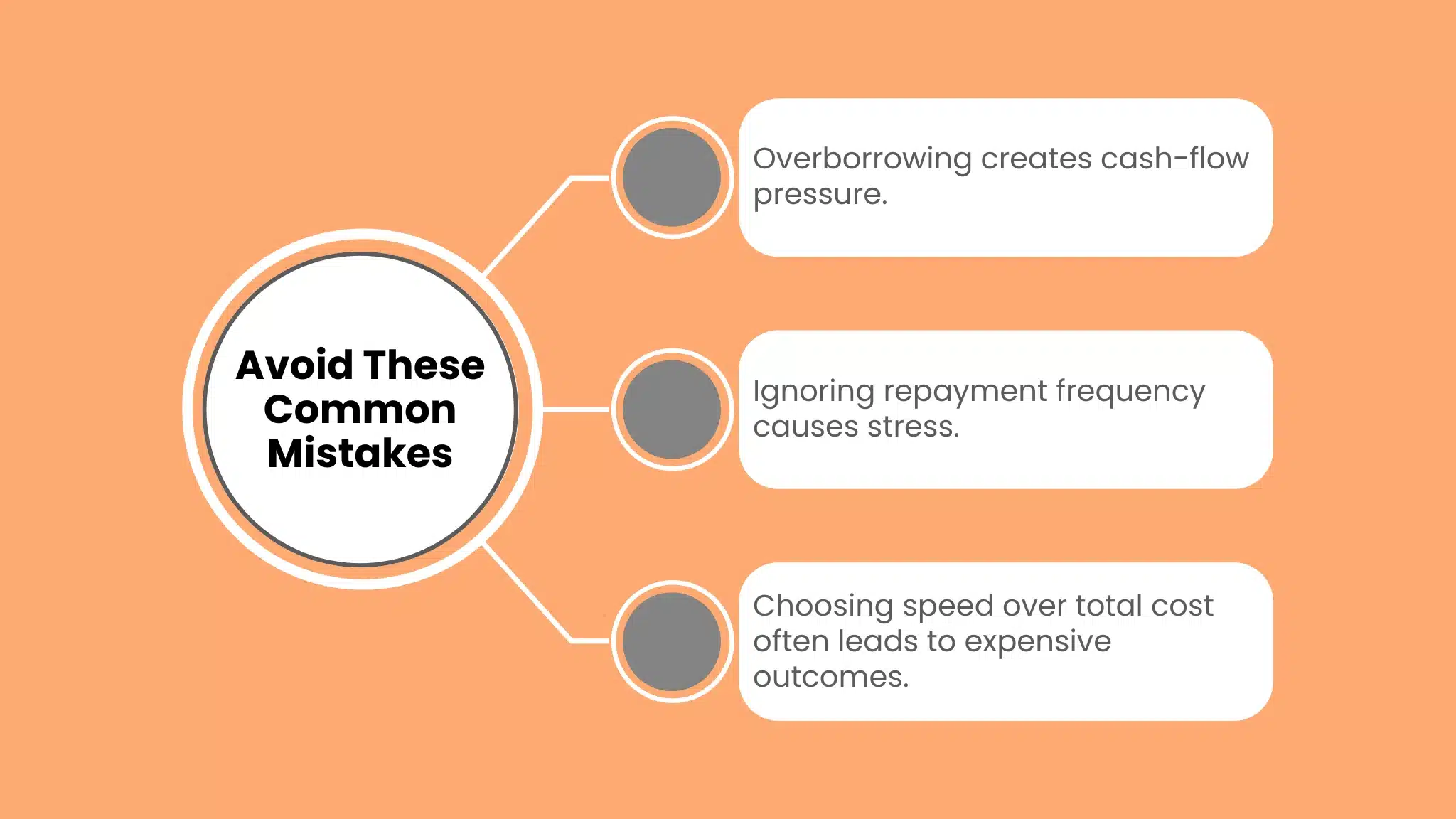

Common mistakes to avoid

Even good funding can go wrong if you move too fast.

So, watch out for these traps:

-

Choosing based on speed only, not total cost

-

Ignoring repayment frequency and cash-flow timing

-

Overborrowing before product-market fit

-

Mixing personal and business spending

-

Applying everywhere at once and hurting credit

Still, the smartest approach is simple: pick the right product, borrow only what you can repay, and track ROI closely.

If you’re starting with cards, explore our breakdown of business credit cards for startup businesses to choose a flexible option that fits your stage.

FAQs

What is unsecured business funding for startups?

It’s funding that doesn’t require collateral like property or equipment.

Instead, approval is based on credit, revenue, cash flow, and other business signals.

Can a startup with no revenue get unsecured funding?

Yes, sometimes through business credit cards or startup-friendly programs.

However, approvals often depend heavily on personal credit and income stability.

Is unsecured funding risky for founders?

It can be if payments are too high for your cash flow.

Therefore, choose a repayment plan that fits your monthly reality.

How fast can unsecured funding be received?

Some options fund quickly after approval, especially cards or certain short-term products.

Still, timelines vary based on verification and provider requirements.

What’s the best unsecured funding option for early-stage startups?

Often, it’s a mix: business credit cards for flexibility and a small line of credit if eligible.

Yet, the “best” choice depends on your revenue, credit, and how you’ll use the funds.

Conclusion: v

Unsecured business funding for startups can be a strong tool when you need capital without collateral.

It helps founders move faster, test profitable startup ideas like business ideas for stay-at-home moms, and invest in growth—while keeping assets off the table.

Still, the smartest approach is simple: pick the right product, borrow only what you can repay, and track ROI closely.

When you do that, unsecured funding becomes a stepping stone, not a burden.